Navigating the landscape of personal finance requires a solid understanding of various savings and investment vehicles. Two popular options that often confuse consumers are moneymarket accounts (MMAs) and moneymarket funds (MMFs).

Despite their similar names, these financial products serve different purposes and come with distinct features, risks, and returns. This article delves into the nuances of each option, helping you make informed decisions that align with your financial goals.

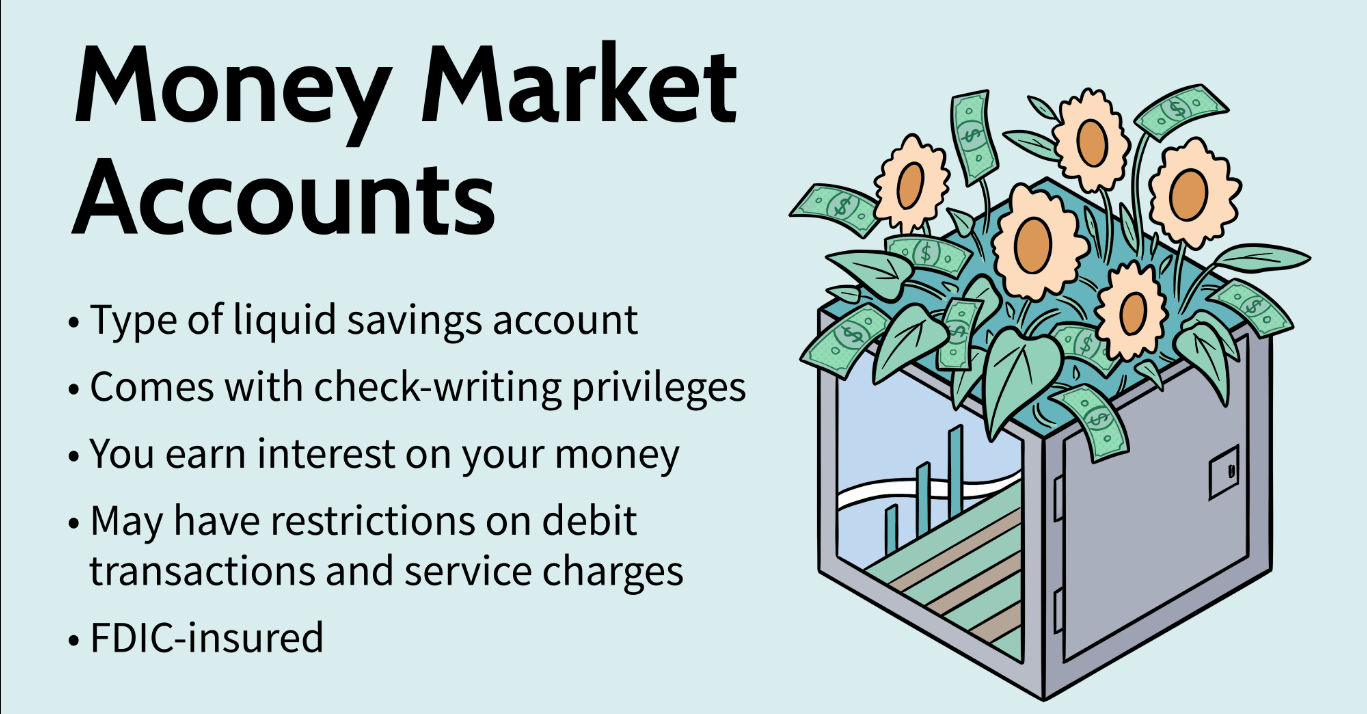

What Is A Money Market Account?

A money market account can be best described as a hybrid between a checking account and a savings account. Offered by banks and credit unions, MMAs combine the benefits of interest-bearing savings with the flexibility of checking features.

Key Features

- Interest Rates: Money market accounts typically earn higher interest rates than traditional savings accounts, making them a viable option for those seeking to maximize their returns.

- Accessibility: With features like debit cards and check-writing privileges, MMAs provide easier access to funds compared to standard savings accounts. You can make deposits and withdrawals without penalties, although some institutions may impose limits.

- Insurance: MMAs are insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) up to $250,000 per depositor, per ownership category. This insurance provides peace of mind for savers concerned about losing their money.

How Does A Money Market Account Work?

Money market accounts function similarly to savings accounts but with added flexibility.

You can deposit and withdraw money at any time, although most accounts limit the number of withdrawals or transfers to six per month. Be sure to check your bank’s specific rules regarding transaction limits and fees.

When To Choose A Money Market Account

MMAs are ideal for those seeking flexible access to their savings for significant purchases or emergencies. For instance, if you are saving for a home renovation or an emergency fund, an MMA allows you to earn interest while keeping your funds accessible.

Real-Life Scenarios

Imagine you have $5,000 saved for unexpected expenses. By placing this amount in a money market account that offers a 4.5% interest rate, you could earn $225 in interest over a year. This growth, coupled with easy access, makes MMAs attractive for emergency savings.

Read More: Debit Card, Cash, Forex - Understanding The Differences

What Is A Money Market Fund?

A money market fund is an investment product that pools money from multiple investors to purchase short-term, low-risk securities such as U.S.

Treasury bills, municipal bonds, and commercial paper. These funds are designed to provide a safe place for investors to earn returns with relatively low volatility.

Key Features

- Types of Securities: Money market funds invest in government securities, corporate bonds, and other short-term investments, aiming to provide a conservative return while preserving capital.

- Accessibility: Unlike MMAs, MMFs typically do not offer debit cards or check-writing privileges. You can redeem your shares and withdraw funds, but this process may take a few days, as transactions are processed through your brokerage account.

- Tax Implications: Some money market funds, particularly municipal funds, can offer tax-free earnings, making them attractive for investors in higher tax brackets.

How Does A Money Market Fund Work?

Investors can purchase shares in money market funds through brokerage accounts. The fund managers aim to keep the net asset value (NAV)close to $1 per share, although there is a risk, albeit small, that the fund may "break the buck" and fall below this value during significant market events.

When To Choose A Money Market Fund

Money market funds are suitable for individuals looking for a place to temporarily hold cash before investing in more volatile assets.

They offer potentially higher returns than traditional savings options and are particularly attractive for those who do not require immediate access to their funds.

Real-Life Scenarios

Suppose you invest $1,000 in a money market fund offering a 5% return. After a year, you would have earned $50. However, if the fund has an expense ratio of 0.15%, your net return would be $48.50.

While MMFs may present a higher yield, the accessibility is less immediate than that of MMAs.

Related: What Is An Investor?

Key Differences Between Money Market Accounts And Funds

Understanding the key differences between MMAs and MMFs is crucial for making informed financial decisions. Here’s a comparison of their essential features:

| Features | Details |

| Safety | Money Market Accounts are FDIC or NCUA insured up to $250,000. Money Market Funds are SIPC insured but not against loss. |

| Opening | Money Market Accounts are opened through banks or credit unions. Money Market Funds are opened at brokerage firms. |

| Minimums | Money Market Accounts' minimums vary by institution and can be high. Money Market Funds generally have low minimum investment requirements. |

| Access | Money Market Accounts offer debit cards and check-writing privileges. Money Market Funds are limited to fund transactions. |

| Interest | Money Market Accounts have fixed interest rates. Money Market Funds offer fluctuating returns based on market conditions. |

| Liquidity | Money Market Accounts are limited to up to six withdrawals per month. Money Market Funds allow unlimited transactions, but processing delays may occur. |

| Fees | Money Market Accounts may charge maintenance fees. Money Market Funds charge management fees (expense ratio). |

Accessibility And Availability

Money market accounts typically provide immediate access to your funds, making them more suitable for day-to-day expenses and emergencies. In contrast, money market funds may require time for withdrawals, impacting liquidity.

Risk Levels

While both MMAs and MMFs are generally considered low-risk, MMAs offer the added security of federal insurance, whereas MMFs do not guarantee protection against principal loss. This makes MMAs a safer option for risk-averse investors.

See Also: Top B2B Marketing Secrets Revealed In <year>

Considerations For Choosing Between MMAs And MMFs

When deciding between a money market account and a money market fund, consider the following factors:

Assessing Your Financial Goals

Identify what you want to achieve with your savings or investments. If you prioritize safety and liquidity, an MMA may be more suitable. If you are willing to accept some risk for potentially higher returns, an MMF could be the better choice.

Understanding Your Risk Tolerance

Evaluate your comfort level with risk. MMAs provide a safe haven for your money with insurance, while MMFs may expose you to slight risks associated with market fluctuations.

Comparing Yields And Fees

Carefully examine the interest rates and fees associated with both options. An MMA may offer a stable return, but it might not compete with the higher yields available from MMFs, which can also have management fees that impact overall returns.

Investment Strategies

Consider incorporating money market funds into a diversified portfolio as a temporary holding place for cash while awaiting more significant investment opportunities.

Resources And Tools

To help you assess your options further, consider using online calculators or tools to compare interest rates, calculate potential earnings, and evaluate your risk tolerance. Websites like Bankrateor NerdWalletcan provide valuable insights into current offerings and rates.

FAQs About Money Market Accounts And Funds

What Is The Main Difference Between A Money Market Account And A Money Market Fund?

Money market accounts are interest-bearing bank accounts that provide liquidity and are insured by the FDIC or NCUA, while money market funds are investment products that pool money to invest in short-term securities and are not federally insured.

Are Money Market Accounts Insured?

Yes, money market accounts are insured by the FDIC or NCUA up to $250,000 per depositor.

How Do I Choose Between A Money Market Account And A Money Market Fund?

Consider your financial goals, risk tolerance, and need for liquidity. If you require immediate access to funds with minimal risk, an MMA may be preferable. If you seek higher returns and are willing to accept some risk, an MMF could be suitable.

Can I Lose Money In A Money Market Fund?

While money market funds are generally low-risk, they are not insured, so there is a potential for loss, particularly in volatile market conditions.

Are Money Market Funds A Form Of Mutual Fund?

Yes, money market funds are a type of mutual fund that invests in low-volatility securities like U.S. Treasury bonds and municipal and corporate securities.

Conclusion

Choosing between a money market account and a money market fund involves careful consideration of your financial goals, risk tolerance, and accessibility needs.

Money market accounts offer safety and easy access, making them ideal for emergency savings and short-term goals.

In contrast, money market funds provide the potential for higher returns, appealing to those willing to accept slight risks.

By understanding the nuances of both options, you can make informed decisions that align with your overall financial strategy.

Always assess your personal financial situation and consult with a financial advisor if needed to ensure you choose the best option for your needs.